Bnei Baruch Finances: Amutot, Family Control, and Reporting

Where you are in the dossier: Money, family, privilege Mixed evidence

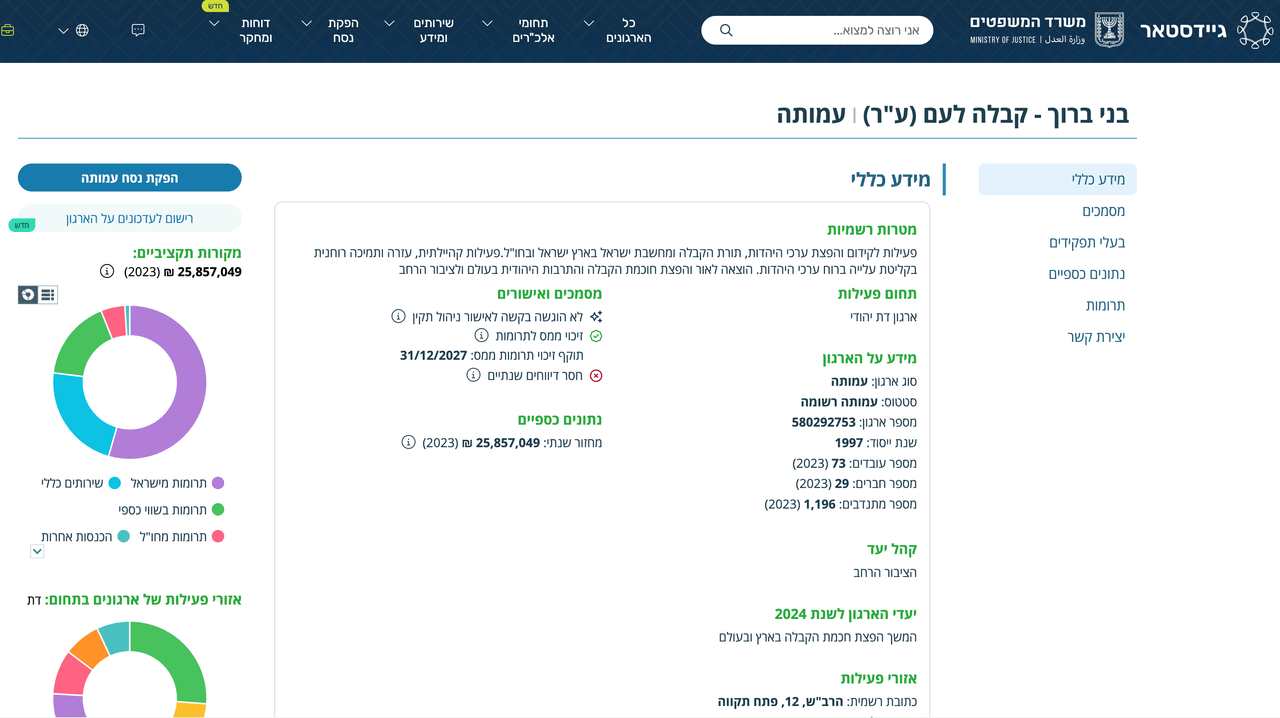

In these photos, we see so-called “official” nonprofits listed on GuideStar, created by Laitman’s structure not for good purposes, but as a tool to conceal real income and evade taxes. With a declared budget of 25 million shekels, the organization not only does not need money — it continues to cynically solicit new donations from its followers, hiding behind “internal projects.”

Publicly, Bnei Baruch describes itself as a spiritual and educational community. Registry records, state audit materials, and The Seventh Eye’s investigation show another record: related amutot, recurring managers, relatives in organizational filings, donations, tithes, and access to money held inside a narrow circle.

Several nonprofit organizations are not, by themselves, proof of wrongdoing. The concern comes from the combination: maaser as a recurring payment, unpaid labor, weak consolidated reporting, family roles, the same functionaries appearing across different amutot, and formal criticism by Israel’s Registrar of Nonprofit Organizations. In December 2024, The Seventh Eye estimated the association’s turnover at almost 25 million shekels a year and separately identified tithing and major donors as substantial sources of funds.

The paper trail is concrete: GuideStar records, officeholders, the audit PDF, payments, and labor. A separate internal meal document is best read in the article on paid communal meals, the visible lifestyle gap in the piece on Mushi Sanilevich, and the later state-resource question in the political-budget article.

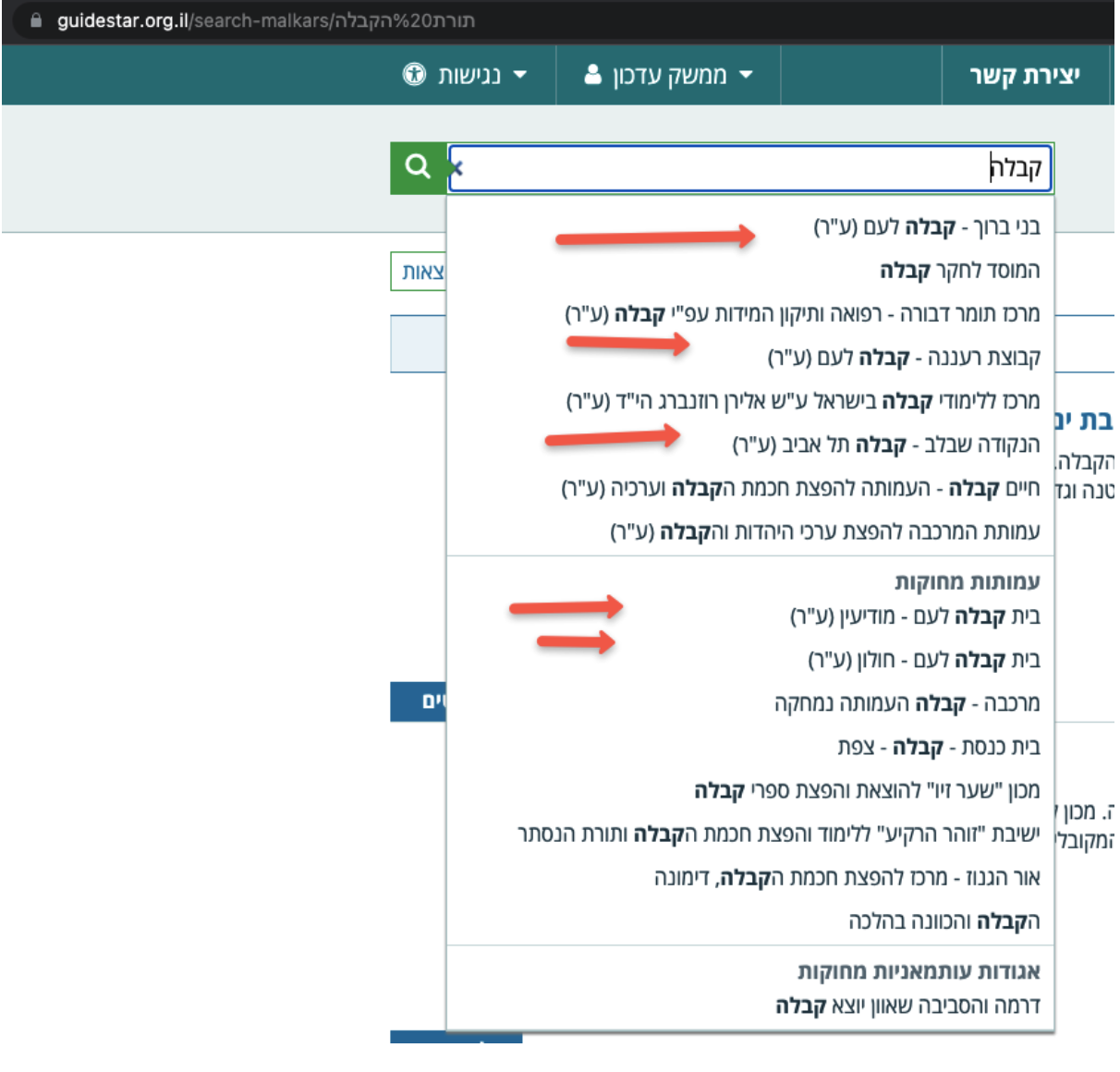

A Network of Amutot and Distributed Reporting

GuideStar lists Bnei Baruch’s parent organization alongside a network of related amutot. Income, expenses, staffing decisions, and legal responsibility are spread across several bodies, so donors do not see a single picture of the resources. Scale matters: according to The Seventh Eye, the Kabbalah La'Am complex in Petah Tikva was purchased in 2013 for about 30 million shekels and includes a lesson hall, studio, offices, early-childhood facilities, and Laitman’s residential unit.

That same year, the movement turned to its own followers for the purchase money. In the autumn of 2013 it released a video appeal, “Bnei Baruch asking” (YouTube, November 2013): the presenter, Shimon Karmon, walks through the headquarters and asks students to “be partners” in the purchase: to buy, not rent, “our own home,” so that everyone would “feel it’s your own place because you took part in buying it.” The language is co-ownership. Legally, a donor to an Israeli amuta receives nothing: no share, no title, no line on the officeholder card. The “common home” that the rank and file pay for stays with the same structure that lists Laitman’s daughter on the parent amuta’s card and houses the leader’s private residence. And the drive ran on a familiar pressure: “we have no time,” “a rare opportunity,” “the world is waiting.” It is the same urgent-mission register Laitman uses to sell the rest of his ideas.

For an organization that collects donations, internal payments, and unpaid labor, this fragmentation complicates oversight. Inside, a participant sees one spiritual movement. In the records, the same participant meets a set of separate legal entities, making income, expenses, assets, and responsibility harder to reconstruct.

What the Guidestar data shows

The central entity remains Bnei Baruch - Kabbalah La'Am (580292753), through which, based on available data, the main financial flow appears to pass. The officeholder card of the parent amutah lists Rachel Laitman, Michael Laitman’s younger daughter. That is a direct fact of family presence inside the organization that appears to carry the main money flow.

This photo shows Rachel Laitman (the youngest daughter and an open lesbian) surrounded by friends from the LGBT community. Although Laitman forced her into marriage, this doesn't guarantee that the genie, driven back, won't want to fly out, having initially deceived her fiancé, Shai Livnat, after destroying the family.

Around the parent amutah are related registry cards: Tel Aviv (organization, officeholders), Ra’anana (organization, officeholders), Be’er Sheva (organization, officeholders), Netanya and Sharon (organization, officeholders), Nazareth Illit (organization, officeholders), Rishon LeZion (organization, officeholders), and Ha-Lev Mevin (organization, officeholders). Closed entities in Hadera (580537868) and Holon (580536357) also remain visible in the same orbit.

One row of registry cards shows two things at once: there are many amutot, and the human circle repeats. Among the officeholders listed across these entities are Ahuva Lubich, Efraim Shiubitz, Ronen Asaf Asias, Ora Ariel, Reuven Ariel, Yaakov Mordechai Ifergan, Dror Ovadya Rabi, and Moshe Yerushalmi. Repeated names do not automatically prove a violation, but they break the image of independent regional bodies. If some amutot were closed, the direct question remains: where did their assets go, who decided that, and what did donors hear about it?

How participation in the movement is monetized

Bnei Baruch’s money comes through several inputs. One, according to former participants, is maaser, the tithe expected from those seeking deeper inclusion in the movement’s inner life. Financially, it is a recurring payment that ties spiritual belonging to the organization’s cash flow. According to Rafaeli’s counter-letter attached to the lawsuit against him, the required payments reached as far as Likud enrollment fees; that document is examined in the article on silenced testimonies.

Additional collections follow the same pattern. Participants hear about difficulties, urgent needs, projects, or events, and another donation round begins. Internal life is also monetized: congresses, communal meals, trips, and other activities framed as part of the spiritual environment bring in revenue. The meal-payment document is examined separately in the article on paid seudot.

Mass unpaid labor is the other major input. Translation, logistics, technical support, event organization, and media production depend heavily on volunteers. At the same time, financial statements and audit materials suggest that some official employees are paid at or near the legal minimum. Participants bring money, free work, and loyalty; access to resources stays with the management circle.

What the state audit documented

The main document is the report of the Israeli Registrar of Nonprofits. It moves the discussion out of ideological accusation and into formal failures recorded by a state authority.

The existence of the report does not automatically create a criminal conclusion on every point. But the criticism no longer comes only from former participants or journalists. The regulator points to concrete failures in procedure, reporting, staffing decisions, and mandatory disclosure.

Concentration of decisions outside formal procedures

The audit materials indicate that major decisions were taken within a narrow circle linked to the movement’s leadership, rather than through functioning collegial procedures. The report gives particular attention to the hiring of relatives and to missing protocols that should have documented discussion and approval of such decisions.

For a nonprofit entity, this is a basic governance failure. If key appointments and financially significant decisions bypass formal discussion, independent oversight loses its force. In such a setting, boards and committees risk becoming decoration around decisions already made elsewhere.

A broken system of financial control

The audit also describes serious failures in the accounting system itself. The report refers to non-functioning or non-existent finance and audit committees, weak separation of duties, and situations in which the same individuals were connected to incoming donations, document registration, and bookkeeping. For any organization dependent on donations, that sharply increases the risk of manipulation, error, and concealed movement of funds.

The auditors also point to problems in the documentation of incoming funds. They note delays in issuing receipts, broken numbering practices, weak handling of cash, and a lack of timely bank reconciliations. A separate block of criticism concerns the treatment of spending on printed and media products. When such costs are written off immediately as current expenses without proper inventory treatment, the financial picture is distorted and it becomes harder to understand how the organization’s resources are actually being allocated.

Violations affecting workers

Another part of the audit findings concerns workers. The review identified failures in time-sheet management, discrepancies between actual payments and contractual terms, and delays in salaries and termination-related compensation. The report also mentions interest-free loans granted on preferential terms to selected employees without proper board approval.

That creates a hard contrast inside one organization: some people face delayed payments and unclear conditions, while others receive favorable loans without proper approval by the board.

Concealment of information that should have been disclosed

The Registrar’s report also states that Bnei Baruch failed to declare large one-time donations and omitted part of the information concerning a sharp increase in the number of volunteers. For a movement that systematically raises money, that strikes directly at donor trust: participants and donors do not see the full volume of money, labor, and resources.

The same report also points to problems with real-estate registration and transfers of funds to other nonprofit entities in the network outside the relevant instructions. The evidence converges on concrete points: relatives, protocols, receipts, cash, wages, loans, large donations, volunteers, real estate, and transfers between amutot.

Why the movement needs so many legal shells

In practical terms, the distributed network of amutot can do several things at once. It disperses outside attention, allows separate reporting, weakens the perception of a single financial center, and makes it difficult to quickly estimate the movement’s total resources. A donor or participant may see only one segment of interaction with the organization, while real turnover and assets are spread across several legal shells.

Multiple amutot become a way to manage information about money. Ideologically, the movement speaks as one spiritual body; financially, it is filed as a network of linked organizations.

How financial resources turn into political influence

Money and discipline create a base for access to state resources. The Seventh Eye reported internal materials describing the “ambassadors” plan in state institutions as a way to “protect the home” and gain a foothold in the education system. The political and budget layer of that story is examined separately in the article on state resources.

Conclusion: a spiritual movement or a distributed financial machine

If the amutot registry, Laitman’s daughter in the parent organization’s filings, the 30 million shekel building (with a fundraising drive aimed at the students themselves), almost 25 million shekels in annual turnover, tithing, paid internal practices, volunteer labor, and the audit PDF are read together, Bnei Baruch is hard to describe as only a spiritual or educational association. The documents show a financial machine wrapped in religious language.

In that machine, money, loyalty, and human labor become linked resources. At the entrance are donations, maaser, unpaid work, and paid internal practices. At the top are the family circle, recurring functionaries, real estate, weak reporting, and a state audit with specific violations.