Bnei Baruch's Financial Architecture: A Network of Amutot, Family Control, and a Lack of Transparency

Bnei Baruch’s Financial Architecture: A Network of Amutot, Family Control, and a Lack of Transparency

Bnei Baruch’s financial model matters not only in itself, but as a key to understanding how the movement sustains organizational discipline, internal hierarchy, and political ambition. Publicly, the structure presents itself as a spiritual and educational community. Yet registry records and state audit materials point to a different reality: not one transparent legal entity, but a network of interconnected amutot, a distributed management structure, and a regime in which access to money and decision-making is concentrated in a narrow circle.

The mere existence of multiple nonprofit entities is not, by itself, proof of wrongdoing. But in Bnei Baruch’s case, what matters is the combination of factors: maaser payments expected from the inner circle, heavy reliance on unpaid labor, the absence of a clear consolidated financial picture, the involvement of relatives and loyal insiders in key management roles, and, finally, the formal criticisms documented by the Israeli Registrar of Nonprofits. In that context, the question is no longer whether the movement has money. The question is how that money is collected, distributed, and kept from the people who provide it.

This article looks at Bnei Baruch’s financial contour as a system. It combines Guidestar data, information on officeholders, the findings of the state audit, and reporting on the commercialization of internal practices, including the article on monetized communal meals, the piece on the family’s operational center, and reporting on the political advancement of people linked to the movement.

A network of amutot as a way to distribute the financial structure

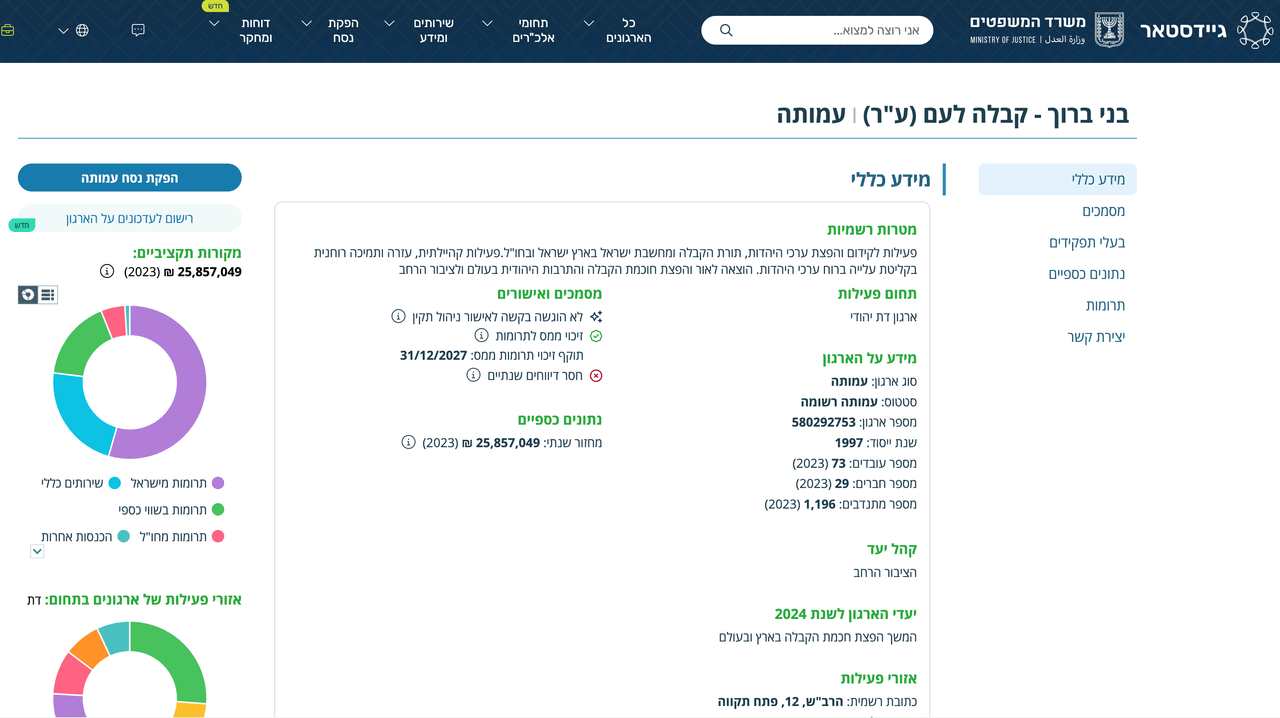

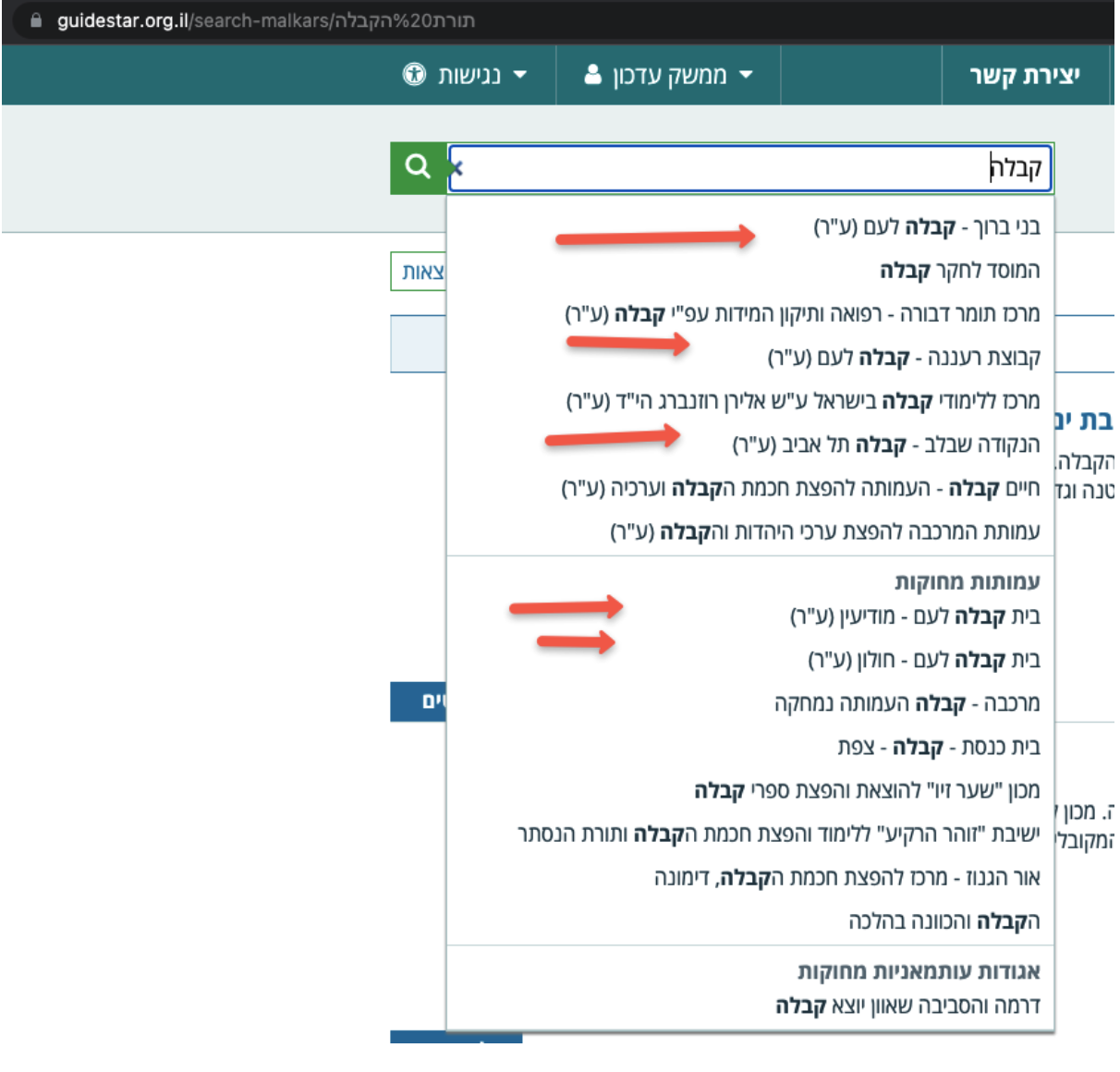

According to Israel’s Guidestar registry, Bnei Baruch does not operate through a single central organization, but through an extended network of amutot. For an outside observer, that means the movement’s financial picture is not visible at a glance. Income, expenses, staffing decisions, and legal responsibility are spread across multiple entities, making a holistic audit far more difficult and leaving the question of where the main resources ultimately accumulate harder to answer.

This architecture matters even more when an organization depends simultaneously on donations, expected internal payments, and free labor. In such a setting, multiple legal entities do not merely allow separate reporting. They also distribute responsibility. For an ordinary participant, the movement appears as one spiritual environment. On paper, however, it is a collection of separate organizations between which it is difficult to reconstruct a single picture of income, expenses, and assets.

What the Guidestar data shows

The central structure remains Bnei Baruch - Kabbalah La-Am (580292753), through which, based on available data, the main financial flow appears to pass. Around it sits a network of associated entities registered in different cities: Tel Aviv (580541555), Ra’anana (580538544), Be’er Sheva (580538130), Netanya and Sharon (580539195), Nazareth Illit (580563013), and Rishon LeZion (580546844). A more specialized body, Ha-Lev Mevin (580537835), also appears within this network.

It is equally revealing that some entities in this network are later dissolved. In the registry, one can see, for example, organizations in Hadera (580537868) and Holon (580536357), both of which are no longer active. Formally, dissolving an amutah should involve transferring its assets to an organization with similar goals. Within a dense internal network, that creates an additional layer of opacity: the assets do not disappear, but are likely redistributed inside the same organizational orbit without any meaningful explanation to donors or rank-and-file participants.

Who controls these structures

If the financial scheme is distributed across several amutot, the next question concerns not the names of the entities but the people who sign documents, make decisions, and bear legal responsibility. This is where it becomes clear that formal fragmentation does not equal genuine independence.

The parent organization and the family circle

The leadership card of the parent organization identifies the officeholders running Bnei Baruch’s main organizational structure. Of particular significance is the role of Rachel Laitman, Michael Laitman’s younger daughter. In financial analysis, this matters not as a biographical footnote, but as a sign of concentrated control within the family circle. When the leader’s relatives participate in the management of key financial flows, the movement begins to resemble not a public or educational structure with independent procedures, but a closed system of internal allocation and control.

That feature is especially significant against the movement’s public rhetoric about spiritual equality, selflessness, and service to a common purpose. The more heavily an organization depends on ideological mobilization and personal devotion, the higher the expected standard of transparency and the clearer the separation should be between the leader’s personal power and the management of financial resources. In Bnei Baruch’s case, the documents suggest the opposite: the financial center is not separated from the leadership’s inner circle, but embedded inside it.

A recurring circle of functionaries across regional amutot

The same pattern appears in other parts of the network. The registry pages for the Tel Aviv amutah, the Ra’anana structure, Ha-Lev Mevin, the Beer Sheva organization, Netanya and Sharon, Nazareth Illit, and Rishon LeZion show the repetition of names and roles. Among the officeholders listed across these entities are Ahuva Lubich, Efraim Shiubitz, Ronen Asaf Asias, Ora Ariel, Reuven Ariel, Yaakov Mordechai Ifergan, Dror Ovadya Rabi, and Moshe Yerushalmi.

The presence of the same people in several nonprofit bodies is not impossible in other settings. But here it functions as an indicator of a single decision-making center. When the network appears decentralized only on paper, while the same functionaries move between key positions, what exists is no longer a set of independent civic initiatives, but a distributed mechanism for managing the same movement.

How participation in the movement is monetized

Bnei Baruch’s financial base is built not on one source, but on a combination of several stable mechanisms. The first, according to many former participants, is maaser, the tithe expected from those seeking deeper inclusion in the movement’s inner life. In that setting, it does not function as a spontaneous charitable gift, but as a disciplinary norm linking spiritual belonging to a recurring financial deduction.

The second mechanism is the constant cycle of supplementary collections. Participants are told about the movement’s difficulties, its urgent needs, or the importance of a new project or event, after which another round of donations begins. The third involves the commercialization of internal forms of communal life. Congresses, shared meals, trips, and other activities formally framed as part of the spiritual environment also function as sources of revenue. This is visible, for example, in the story of communal meals turned into an income stream, where an internal practice gradually becomes a paid service without meaningful financial reporting to the participants themselves.

The fourth element, without which the whole model would not function at this scale, is mass unpaid labor. Translation, logistics, technical support, event organization, and media production depend heavily on volunteers. At the same time, financial and audit materials suggest that some official employees are paid at or near the legal minimum. From an investigative perspective, that combination is critical: participants contribute money, labor, and loyalty, while real access to resources is concentrated in a narrow circle of managers.

What the state audit documented

The central question in this investigation is not whether Bnei Baruch’s model can be interpreted critically, but what has been documented formally. In that respect, the key source is the report of the Israeli Registrar of Nonprofits. Its importance lies in moving the discussion out of the realm of ideological accusation and into the realm of formal failures recorded by a state authority.

The existence of such a report does not automatically amount to a criminal conclusion on every point. But its significance is difficult to overstate. It shows that concerns about the movement’s financial and managerial discipline do not come only from former participants or journalists. They also appear in a formal review in which the regulator points to concrete failures in procedure, reporting, staffing decisions, and mandatory disclosure.

Concentration of decisions outside formal procedures

The audit materials indicate that major decisions were taken not through functioning collegial mechanisms, but within a narrow circle linked to the movement’s leadership. Particular attention is given to the hiring of relatives and the absence of proper protocols that should have documented discussion and approval of such decisions.

For a nonprofit entity, this is not a minor technical issue but a question of basic governance. If key appointments and financially significant decisions bypass formal discussion, the very idea of independent oversight collapses. In such a setting, boards and committees cease to function as supervisory bodies and become little more than decoration around decisions already made elsewhere.

A broken system of financial control

The audit also describes serious failures in the accounting system itself. The report refers to non-functioning or non-existent finance and audit committees, weak separation of duties, and situations in which the same individuals were connected to incoming donations, document registration, and bookkeeping. For any organization dependent on donations, that sharply increases the risk of manipulation, error, and concealed redistribution of funds.

The auditors also highlight problems in the documentation of incoming funds. They note delays in issuing receipts, broken numbering practices, weak handling of cash, and a lack of timely bank reconciliations. A separate block of criticism concerns the treatment of spending on printed and media products. When such costs are written off immediately as current expenses without proper inventory treatment, the financial picture is distorted and it becomes harder to understand how the organization’s resources are actually being allocated.

Violations affecting workers

Another part of the audit findings concerns labor relations. The review identified failures in time-sheet management, discrepancies between actual payments and contractual terms, and delays in salaries and termination-related compensation. Particularly revealing is the mention of interest-free loans granted on preferential terms to selected employees without proper board approval.

From a journalistic standpoint, this matters because it points to more than accounting sloppiness. It reveals an internal hierarchy of access to resources. Some people inside the system face delayed payments and opaque conditions; others benefit from special arrangements that do not resemble standard practice in a transparent nonprofit environment.

Concealment of information that should have been disclosed

Another significant block concerns mandatory disclosure. The Registrar’s report states that Bnei Baruch failed to declare large one-time donations and omitted part of the information concerning a sharp increase in the number of volunteers. For an organization that builds its identity around service to a shared cause and systematically raises money, this has direct implications: participants and donors are not given a full picture of the resources the movement actually commands.

The same report also points to broader issues, including problems with registering real estate and transfers of funds to other nonprofit entities in the network outside the relevant instructions. Considered alongside the amutot network, this suggests that opacity is not confined to one area. It appears across several layers at once: in staffing, documentation, donations, assets, and transfers between affiliated organizations.

Why the movement needs so many legal shells

In practical terms, the distributed network of amutot solves several problems at once. It disperses outside attention, allows separate reporting, weakens the perception of a single financial center, and makes it difficult to quickly estimate the movement’s total resources. A donor or participant may see only one segment of interaction with the organization, while real turnover and assets are spread across several legal shells.

That is why the issue of multiple amutot matters not as a bureaucratic curiosity, but as a method of organizing power. When a movement describes itself ideologically as one spiritual body, but structures itself financially as a scattered network of interlinked organizations, that duality itself becomes an instrument of informational control.

How financial resources turn into political influence

Financial opacity would matter even without the political dimension. But in Bnei Baruch’s case, money and organizational discipline serve not only internal reproduction. They also support the movement’s penetration into state and party structures. The clearest example is Hanoch Milwidsky, the movement’s former legal adviser, who rose to an influential political position in Israel despite serious public allegations and investigations.

At the same time, the structure demonstrated an ability to mobilize supporters inside Likud and to turn disciplined membership into a political instrument. In that light, initiatives such as the bill associated with funding of up to 50 million shekels per year become especially important. Such proposals would open a route to ongoing state financing under the language of educational and employment integration. In that configuration, the movement’s financial structure stops being merely an internal matter and becomes a base for organized lobbying.

Conclusion: a spiritual movement or a distributed financial machine

If one puts together the registry data, the role of the family circle, the model of expected tithing, the commercialization of internal practices, the exploitation of volunteer labor, and the findings of the state audit, it becomes difficult to describe Bnei Baruch purely as a spiritual or educational association. The documents point instead to an organization in which ideological language coexists with a hard financial logic, while access to resources and decisions is concentrated in a recurring circle of people.

That does not mean every element of the network is, by itself, proof of the same specific violation. But taken together they form a stable picture: the movement’s public rhetoric of unity and spiritual purpose serves as a facade for a distributed corporate system in which money, loyalty, and labor are interdependent resources. That is why the issue of finances in Bnei Baruch cannot be treated as secondary. It sits at the center of the broader conversation about power, governance, and the movement’s actual nature.

For a closer look at the movement’s operational center and the lifestyle of its upper tier, see My Wonderful Life.

Sources

The main documents and registry records used in this article are linked directly in the body of the text. The key state source is listed separately below.

Share your story anonymously

Write to us at: LAITMAN.HUI@MAIL.RU